WHAT IS MUTUAL FUND?

A Mutual Fund is just a pipe that connects your savings to a bunch of securities such as stocks and bonds. In simple words, a mutual fund pools money from multiple investors to invest in diversified assets like stocks, bonds, or gold. It’s managed by professionals and offers access to markets without needing deep expertise.

For example, think about a "Shared Taxi/Ride-Share"

Imagine you need to get to a specific destination (financial goal), but a private taxi (buying individual stocks/bonds) is too expensive, or you're unsure of the best route. So, Instead, you opt for a shared taxi or a ride-share service where multiple people going in the same direction so, they chip in for the ride. Everyone contributes a smaller fare. The professional driver (the fund manager) knows the best routes, avoids traffic, and gets everyone to their destination efficiently. You benefit from their expertise without having to navigate yourself. The ride-share company here doesn't just use one type of car; it uses a diverse fleet of vehicles (like different types of stocks and bonds). If one "car" hits traffic, the others in the "fleet" keep moving, spreading out the risk. The concept here is that you're sharing the cost and benefiting from a professionally managed journey that would be less accessible or more costly on your own. You're leveraging shared resources for a common goal. You arrive at your destination effectively and at a lower individual cost than if you'd taken a private ride.

What do you actually own?

Not just the individual stocks or bonds themselves but you own units of the pool that owns them.

- Units = your seat in the shared ride.

- NAV = the meter price per seat.

- Your return = change in NAV + any income (dividends/interest) the fund distributes.

When the value of the underlying investments rises, NAV tends to rise. If markets fall, NAV can fall too. Simple.

How a mutual fund works?

- Money is pooled. Thousands of investors, small and big, add money to the same fund.

- There’s a plan. Every fund has a mandate—e.g., large Indian companies, short-term bonds, or a specific index.

- Pros do the driving. A fund manager and research team buy/sell and keep the portfolio aligned to the plan.

- Daily pricing. The fund calculates and publishes NAV regularly so you always know the per-unit value.

- You can buy or exit. You purchase units at today’s NAV; you redeem units when you need money (check any exit load or timelines).

- It’s transparent. Factsheets and statements show what the fund owns, costs, and performance.

Why people use mutual funds?

- Diversification in one step. Even a small amount gets spread across many securities.

- Professional management. Full-time teams watching markets so you don’t have to.

- Easy to start, easy to maintain. Invest small amounts; automate with SIPs if you like.

- Liquidity. Most funds let you redeem on business days at that day’s NAV.

- Clear rules. Funds operate under regulations and publish regular disclosures.

The team behind your funds:

- AMC (Asset Management Company): Runs the fund and makes day-to-day investment decisions.

- Fund Manager & Research Team: Pick securities, manage risk, rebalance.

- Trustees: Oversee the AMC to ensure it follows the rules and the fund’s mandate.

- Custodian: Safely holds the securities.

- RTA (Registrar & Transfer Agent): Maintains investor records, transactions, and statements.

- Regulator (India: SEBI): Sets the framework and disclosure standards.

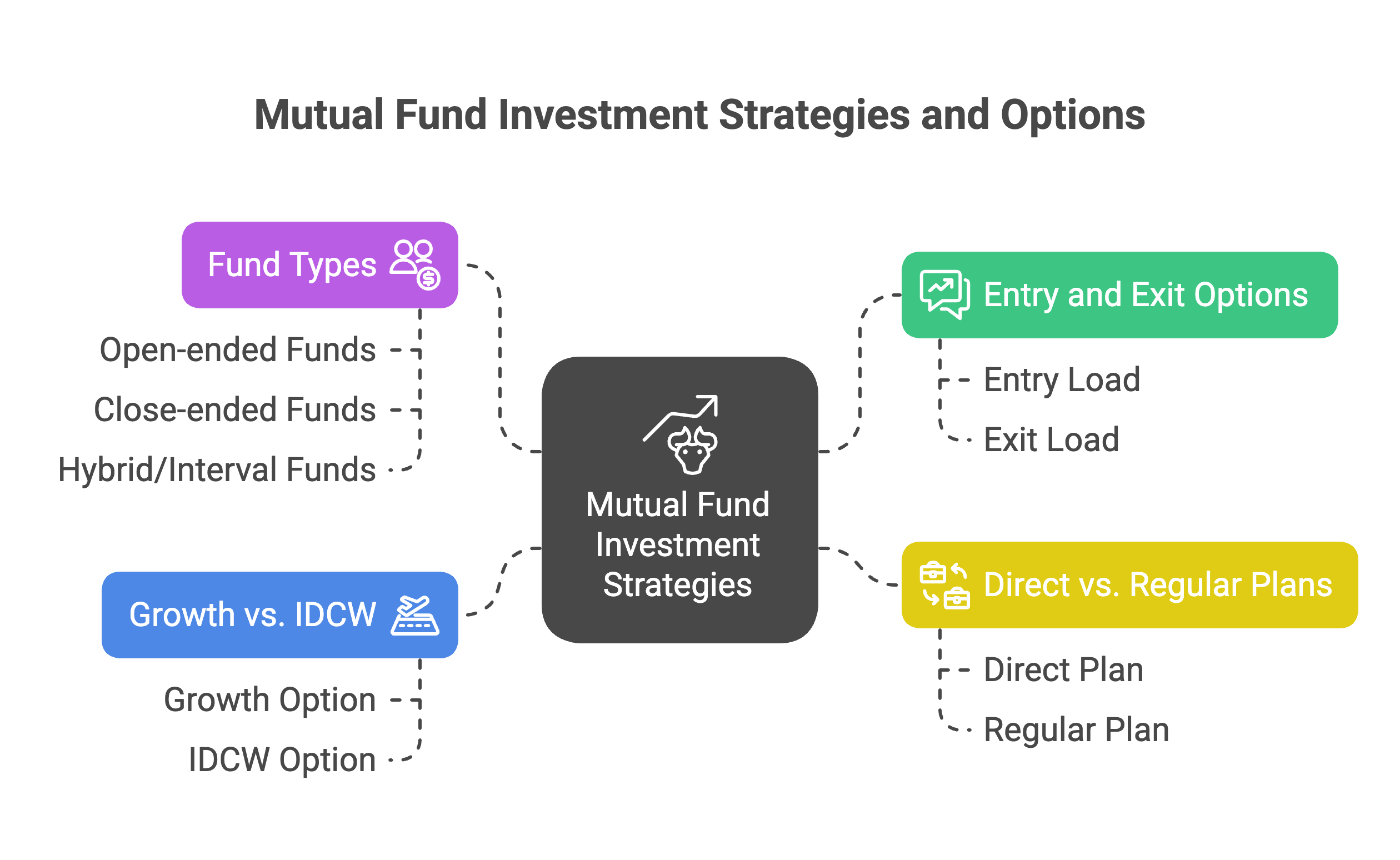

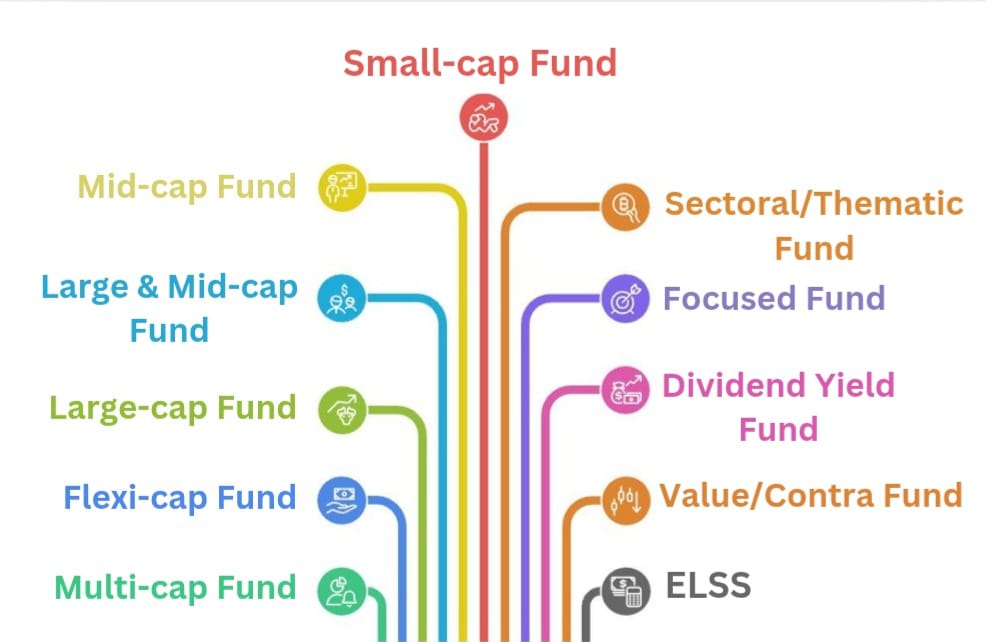

Types of Mutual Fund’s:

- Equity Funds: Aim for growth; higher ups & downs; suited for longer horizons.

- Debt Funds: Aim for stability/income; affected by interest rates & credit quality.

- Hybrid Funds: Mix equity + debt for a smoother ride.

- ETFs: Passive investment schemes.

- Solution-Oriented: Goal-based (e.g., retirement/children) with longer lock-ins.

Myth vs Fact

- Myth: Mutual funds guarantee returns.

Fact: Returns are market-linked and can fluctuate. - Myth: A lower NAV means the fund is “cheaper.”

Fact: NAV is just per-unit math; % return matters, not rupees per unit. - Myth: More funds = more safety.

Fact: Over-diversification can duplicate holdings and dilute results. - Myth: Last year’s top performer is the best choice.

Fact: Chasing winners often backfires; discipline + fit to goal matter more. - Myth: You need a lot of money to start.

Fact: You can begin with small amounts (even a ₹100–₹500 SIP) and scale up comfortably. - Myth: You must be a market expert.

Fact: Mutual funds are professionally managed and publish clear disclosures so you don’t have to micro-analyse every stock or bond. - Myth: Mutual funds are hard to track.

Fact: They’re transparent and well-regulated—daily NAVs, monthly factsheets, audited portfolios, and SEBI oversight. - Myth: SIPs are only for small investors.

Fact: SIP is a discipline tool for any ticket size—great for building wealth steadily and removing timing stress. - Myth: Only equity funds are “real” mutual funds.

Fact: There are equity, debt, hybrid, and index options—so you can match your goal and time horizon precisely. - Myth: More funds = more safety.

Fact: A focused mix of 1–3 distinct funds often given ample diversification without duplication. - Myth: Getting money out is difficult.

Fact: Open-ended funds let you buy/redeem on business days with standard settlement timelines—liquidity is built in.

For an example:

You invest ₹10,000 in a fund with NAV ₹50.

You get 200 units (₹10,000 ÷ ₹50).

If later the NAV is ₹55, your units are worth ₹11,000.

Redeem then (assuming no exit load), you’ll receive about ₹11,000 before any applicable taxes/charges.

This isn’t a prediction. It’s just how units × NAV works.

Open ended or close ended? Know the difference:

- Open-ended funds: Buy/redeem on business days at that day’s NAV (subject to cut-off times and loads, if applicable); money typically credited within standard timelines.

- Closed-ended funds: Fixed tenure or listed units; better for specific use-cases. Most beginners start with open-ended.

Goal-Fit Checklist. Be clear with your goals

A mutual fund likely fits if your goal:

- Has a clear time frame (longer for equity; shorter for debt/liquid),

- Can tolerate ups & downs without panic exits,

- Benefits from diversification and professional management,

- Works with small, regular contributions (SIP) or a clean one-time deployment,

- Needs transparent reporting and easy monitoring.

If you tick 3+ boxes, it’s worth a closer look.

Note (Please Read)

Mutual funds are subject to market risk. Read scheme documents (SID/KIM/factsheet) carefully. Past performance does not guarantee future results. Choose funds that match your goals, time frame, and risk tolerance.

.png)

.png)

.png)

.png)

.png)