The Power of Compounding – The Secret behind your Growing Wealth Effortlessly

Have you ever wondered how some people build large fortunes without taking extreme risks, the answer often lies in one simple concept known as: The Power of Compounding.

It’s not about making quick profits or finding “the next big thing.” It’s about letting time and discipline work for you.

Compounding the “8th Wonder of the World.” Those who understand it, earn it; those who don’t, end up paying for it.

So, let’s have a look and see how it helps in long-term wealth creation.

What is Compounding?

Compounding is what happens when your investments it earns returns, and then those returns are reinvested to generate even more returns.

Your money earns money. Then that money earns more money.

Think of planting a tree — in the first few years, growth is slow. But once the roots are deep, it grows faster, gives more shade, and produces more fruit year after year. That’s how compounding works in your financial life.

How Does Compounding Work?

Here’s a simple example:

You invest ₹1 lakh at 12% annual return.

- After 1 year → ₹1,12,000

- After 2 years → ₹1,25,440

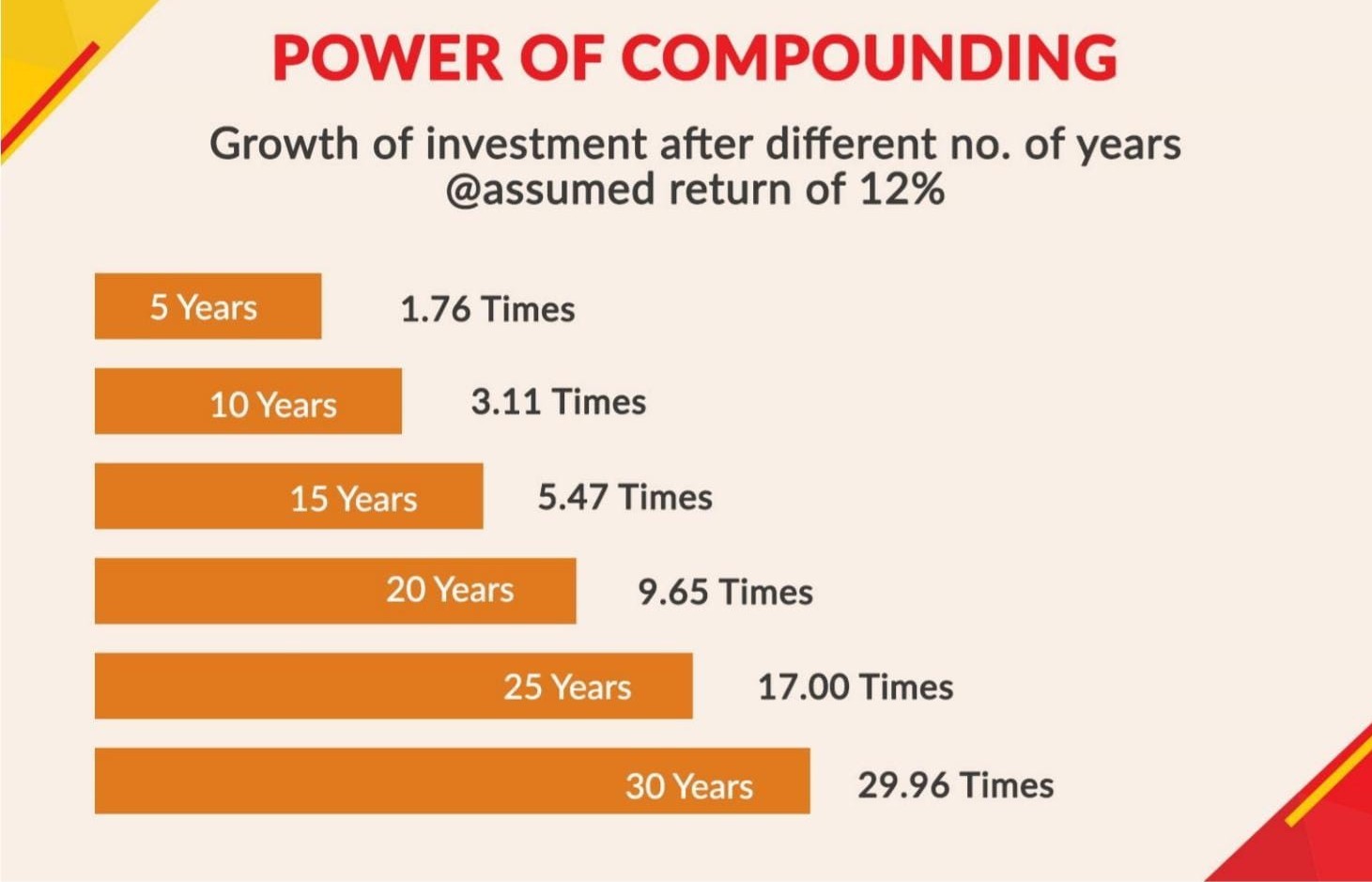

- After 5 years → ₹1.76 lakhs

- After 10 years → ₹3.11 lakhs

- After 30 years → ₹29.96 lakhs

Notice something? The biggest jump happens in the later years. That’s because every rupee you earned earlier is now also earning returns.

Why Compounding is a Game-Changer

- It Multiplies Wealth Over Time

Even modest, regular investments grow into substantial wealth given enough time.

Example: ₹10,000/month @ 12% → ₹3+ crore in 30 years.

- It Works Silently

You don’t need to constantly monitor markets. As long as you stay invested, compounding keeps working behind the scenes.

- It Rewards Patience

The longer you stay invested, the more powerful compounding becomes. It’s like fine wine — it gets better with time.

Golden Rules to Maximize Compounding

- Start Early

Even ₹5,000/month started at age 25 beats ₹10,000/month started at age 35. The extra years make all the difference. - Stay Consistent

The amount you start with matters less than staying disciplined every month. - Don’t Withdraw Prematurely

Interruptions break the compounding chain. Let your money work without disturbance. - Choose the Growth Option in Mutual Funds

This ensures returns are reinvested instead of being paid out, accelerating compounding. - Avoid Timing the Market

Missing just a few of the best market days can hurt returns significantly. “Time in the market” beats “timing the market.”

Why SIPs and Compounding Are Best Friends

A Systematic Investment Plan (SIP) is the perfect way to harness compounding because it combines:

- Regular investing

- Rupee-cost averaging (buy more when prices are low, less when high)

- Long-term discipline

This means you don’t have to guess the right time to invest — you simply keep going, and compounding does the rest.

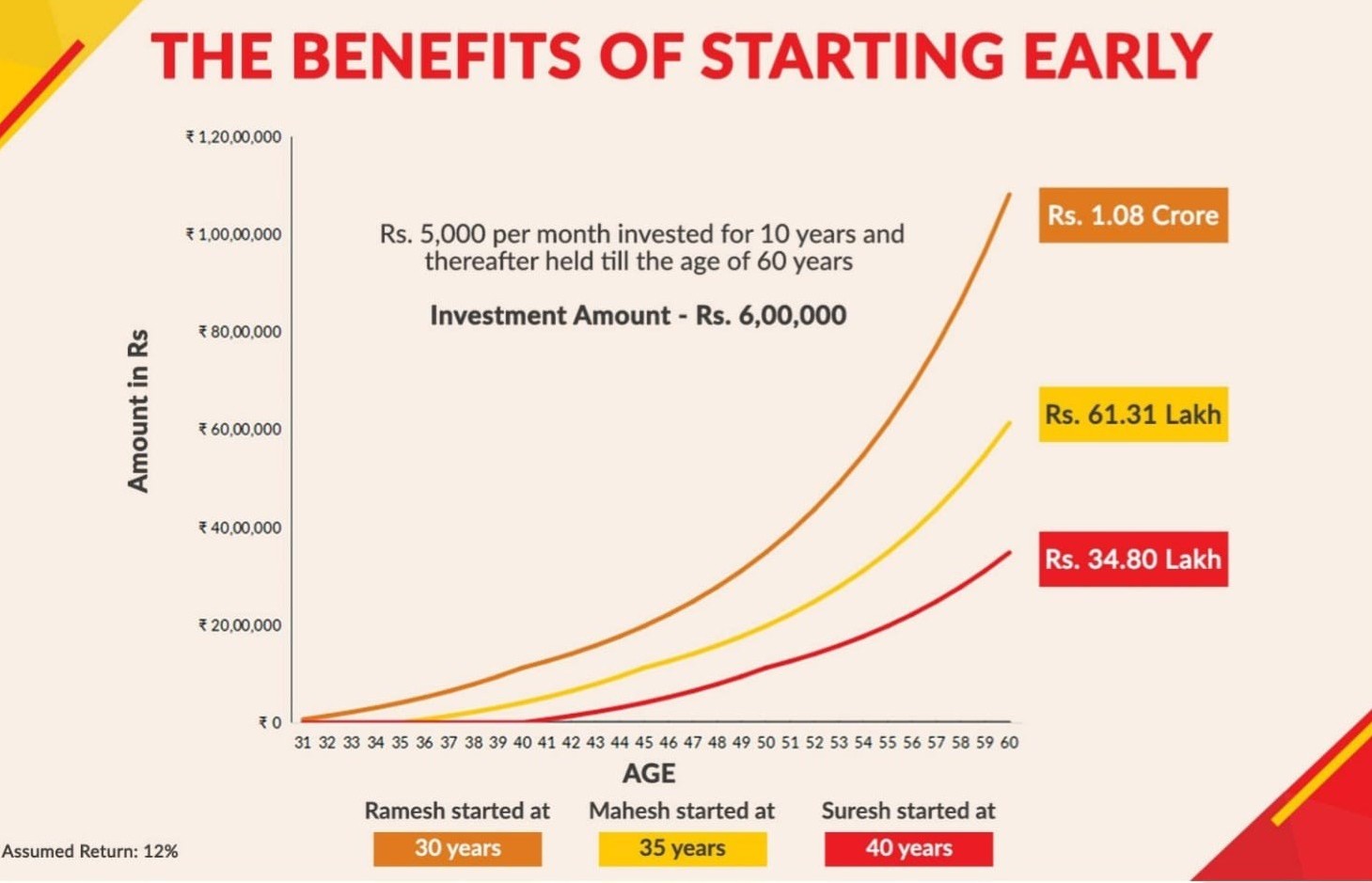

The Magic of Starting Early

Let’s compare two friends, Aarav and Rohit.

- Aarav starts investing ₹5,000/month at age 25 and continues until age 55 (total invested = ₹18 lakh).

- Rohit starts investing ₹5,000/month at age 35 and continues until age 55 (total invested = ₹12 lakh).

Assumption: Both earn the same average annual return of 12%.

At age 55:

- Aarav’s Corpus: ₹1.77 crore

- Rohit’s Corpus: ₹50 lakhs

Result: Aarav ends up with ₹1.27 crore more than Rohit - simply because he started 10 years earlier.

Why?

Those extra 10 years gave Aarav’s early investments more time to grow through the power of compounding, turning small monthly SIPs into massive long-term wealth.

Conclusion:

Compounding is not about luck, timing, or chasing trends. It’s about starting early, staying consistent, and letting time work its magic.

Whether you start with ₹1,000/month or ₹10,000/month, the key is to start now.

Every year you delay, you’re losing potential growth that you can never get back.

Note: Mutual funds are subject to market risks. Read all scheme documents carefully. Past performance is not indicative of future returns.

.png)

.png)

.png)

.png)

.png)