.png)

In the previous blog, we had a complete guide of equity mutual fund from basics, read it now if you haven’t yet.

So, now Will understand other asset classes investment funds, like Debt, hybrid, commodities, international, solution – oriented and passive funds, let’s get Started.

Exploring the world of mutual funds? Feels confusing right? because you have got too many options but think of it like building a well-rounded meal. Each category of fund is an ingredient with a specific purpose, from providing a stable base to adding a bit of flavour and spice. The key is to create a strategic mix that aligns with your financial goals, your timeline, and your comfort with risk.

Let's break down the different types of funds to help you craft your perfect investment plate.

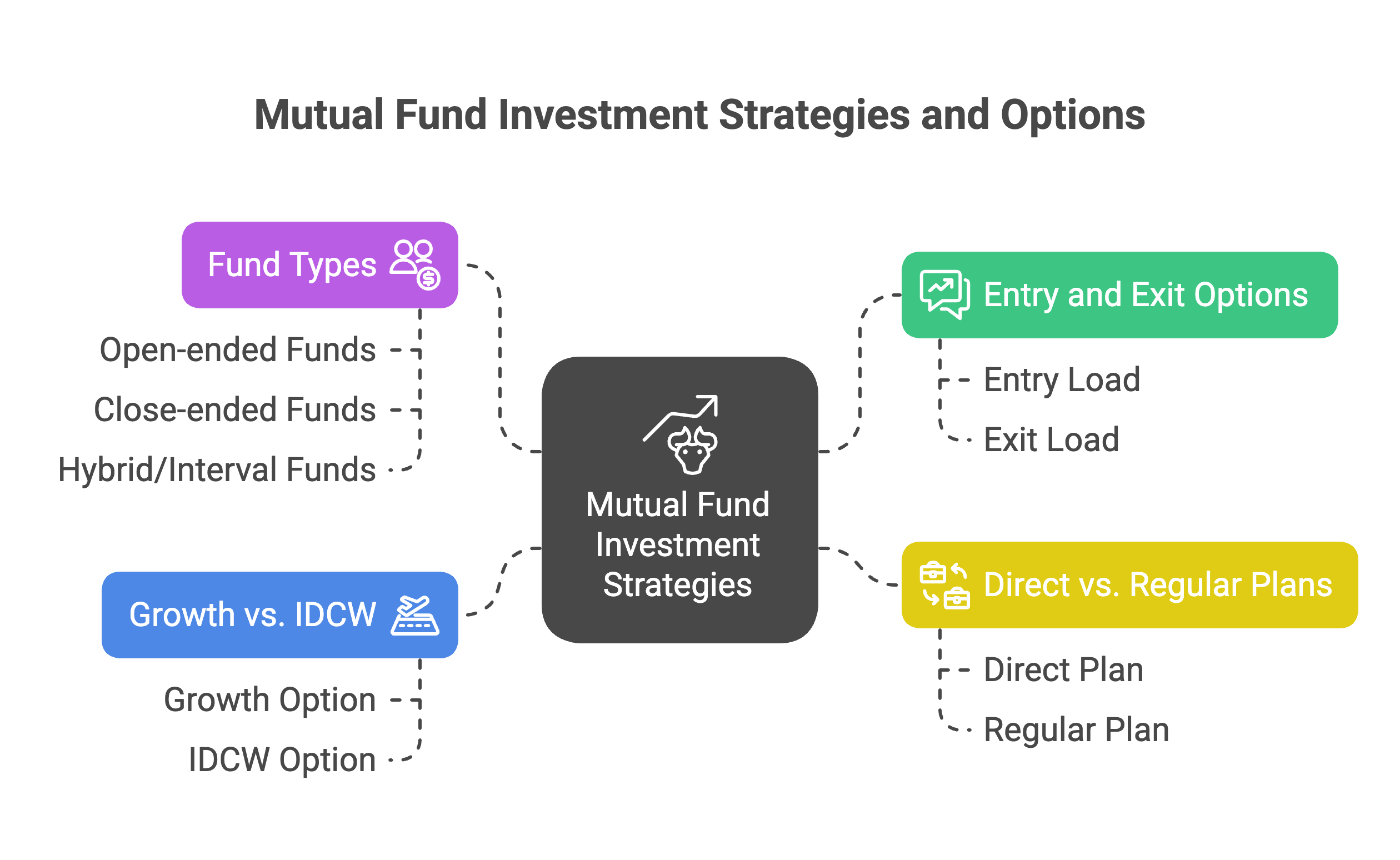

1. Debt Funds: The Safety Net

Debt funds are the "staple" food on your plate, providing stability and regular income. They are less volatile than equity funds and are ideal for short-to-medium-term goals. These funds invest in fixed-income securities like government bonds, corporate bonds, and money market instruments.

When it comes to debt funds, it's crucial to match your investment horizon to the fund's duration. Chasing the highest return can be risky. Remember, a good investment isn't just about high returns; it's about low costs, liquidity, and having access to your money when you need it.

Here's a detail of the different types:

-

Overnight & Liquid Funds: These are the safest options. Overnight funds invest in securities that mature in one day, while liquid funds hold securities with a maturity of up to 91 days. They're perfect for parking cash needed in the immediate future, like an emergency fund or money for a down payment.

Example: You invest ₹10,000 in a liquid fund for 3 months at an annual return of 6%. Your principal will grow by ₹150 (₹10,000 * 6% * 3/12). Your final amount is ₹10,150.

-

Ultra-Short, Low, & Short Duration Funds: These funds are categorized by their Macaulay duration, which measures a bond’s sensitivity to interest rate changes. They're designed for money needed in the short term, typically from 3 months up to 3 years.

-

Medium & Long Duration Funds: For longer time horizons, these funds take on more interest rate risk but can deliver higher returns. As a rule of thumb, use a medium-duration fund for needs 3-4 years away and a long-duration fund for needs over 7 years away.

-

Dynamic Bond Fund: This fund gives the manager the freedom to actively change the portfolio's duration based on their view of interest rate movements. This can be a high-risk category for a new investor because the fund's success depends heavily on the manager's skill.

-

Corporate Bond & Credit Risk Funds: These funds lend to private companies. Corporate bond funds stick to high-rated companies (AA+ and above), while credit risk funds venture into lower-rated bonds (AA and below). The most recent offers the potential for higher returns but comes with a greater credit risk - the risk that the borrower will default. SEBI even changed the name of "credit opportunities" funds to "credit risk" to make this clearer to investors.

Example: You invest ₹10,000 in a corporate bond fund for 3 years, expecting an 8% annual return. Your investment will grow to ₹12,597.

-

Banking & PSU Fund: These funds are considered very safe, as they invest in debt instruments from banks and Public Sector Undertakings (PSUs), which are generally high-quality borrowers.

-

Gilt Funds: For the ultimate safety, these funds invest in government securities (G-Secs), which have zero credit risk.

-

Floater Fund: An innovative choice, this fund invests in floating-rate instruments where the interest rate adjusts to market conditions. This helps hedge against the risk of rising interest rates.

2. Hybrid Funds: The Best of Both equity and debt

Hybrid funds are like a carefully crafted "thali" that balances different elements. They invest in a mix of both equity and debt, aiming to provide steady returns with some protection from market ups and downs.

-

Conservative Hybrid Fund: For the cautious investor. They have a higher allocation to debt (75%-90%) and a smaller allocation to equity (10%-25%). Ideal for steady income with limited stock market exposure.

Example: You invest ₹1,00,000, with 80% in debt (8% return) and 20% in equity (12% return). Your portfolio value would be ₹1,08,800.

-

Aggressive Hybrid Fund: For the moderate risk-taker. These funds invest predominantly in equity (65%-80%) and the rest in debt. They aim for growth while using the debt component to mitigate some risk.

Example: You invest ₹1,00,000, with 75% in equity (15% return) and 25% in debt (8% return). Your portfolio value would be ₹1,13,250.

-

Dynamic Asset Allocation / Balanced Advantage Fund: This is for a hands-off approach. The fund manager dynamically shifts the allocation between equity and debt based on market conditions, aiming to capitalize on market movements.

-

Multi-Asset Allocation Fund: The ultimate diversification tool. These funds invest in at least three different asset classes—such as equity, debt, and gold—with a minimum of 10% in each.

-

Arbitrage Fund: A unique, low-risk strategy. These funds capitalize on the price difference of a stock between the cash and derivatives markets. They are treated as equity funds for tax purposes but have risk characteristics like liquid funds.

-

Equity Savings Fund: A sophisticated option that invests in a combination of equity, debt, and arbitrage, providing a tax-efficient and low-volatility alternative.

3. Passive Funds: The "Fill It, Shut It, Forget It" Approach

-

Index funds and Exchange Traded Funds (ETFs) are part of the "Other Schemes" category and are considered passive funds. Unlike active funds, where a fund manager actively tries to beat a benchmark, passive funds simply mimic a specific index.

-

Think of active funds as a fine-dining restaurant with a celebrity chef who aims to deliver a unique, superior experience for a higher price. Passive funds, on the other hand, are like a reliable chain restaurant known for providing a consistent, standard experience at a low cost.

-

The key benefit of passive funds is that you get the index return without having to manage the individual stocks or bonds yourself. For example, if you bought all 30 stocks on the Sensex or all 50 in the Nifty and held them, you would get the index return, which has been around 14% annually over the last three decades. Passive funds are a great, low-cost option for new investors or those who want a simple, long-term approach to investing.

-

Example: Priya’s Passive Fund: Priya chooses a Nifty 50 Index Fund. This fund simply mirrors the index’s performance. It has a very low fee, say 0.25% (or ₹250).

-

Calculation: Priya’s investment grows by the market’s 10%, which is ₹10,000. After the fund’s fee of ₹250 is deducted, her total return is ₹9,750.

-

Final Amount: Her ₹1,00,000 becomes ₹1,09,750.

4. Specialty & Solution-Oriented Funds

-

Commodity Funds: These funds focus on real assets like gold. Gold funds are popular as a hedge against inflation and a safe-haven asset.

-

International Funds: Your ticket to global markets. These funds invest in companies outside of India, helping you diversify your portfolio and tap into growth opportunities that may not be available domestically. However, they also come with currency and geopolitical risk.

-

Solution-Oriented Funds: Designed for specific life goals like retirement and children's education, these funds have a mandatory 5-year lock-in period. This lock-in can be a useful tool for investors who might otherwise panic and sell during a market downturn.

Conclusion:

The world of mutual funds offers a vast array of choices, but it’s not meant to confuse you—it's designed to give you the tools to build a portfolio that is uniquely yours. Don't just pick a fund; create a strategic mix of equity, debt, and other asset classes that aligns with your financial goals, your timeline, and your comfort level with risk. By understanding these different categories and their characteristics, you can make informed decisions and build a robust, diversified investment portfolio.

.png)

.png)

.png)

.png)